library(tidyverse)Regression

This lesson covers simple and multiple linear regression — the foundational predictive modeling technique in business analytics. Building on the correlation analysis from the previous lesson, we move from describing relationships to modeling and forecasting them. The lesson also covers the assumptions that regression requires, what goes wrong when they are violated, and how to diagnose them systematically in R.

We begin with the simple linear regression model, which estimates a straight-line relationship between one explanatory variable and one continuous response variable. The key outputs are the slope and intercept — parameters that define the regression line — along with three goodness-of-fit measures: the Residual Standard Error (RSE), the coefficient of determination (R²), and the Adjusted R². The F-statistic tests whether the model as a whole explains a meaningful share of the variation in the outcome, and the t-statistics on each coefficient test each predictor individually.

We then extend to multiple regression, which adds two or more explanatory variables to the model. Multiple regression allows us to control for competing influences on the outcome, isolating the unique contribution of each predictor while holding the others constant. We cover the p-value method for variable selection — iteratively removing the least significant predictors while watching that the Adjusted R² does not meaningfully decline — and multicollinearity, which arises when predictors are highly correlated with each other and can distort or destabilize coefficient estimates.

The lesson closes with regression using categorical variables and a dedicated section on regression assumptions. When a predictor is categorical rather than continuous, R automatically converts it into dummy variables — a set of binary indicators, one per category, with one category held back as the reference. We work through examples with two-category and multi-category predictors, and combine continuous and categorical predictors in the same model. The assumptions section covers linearity, independence of errors, homoscedasticity, normality of residuals, and multicollinearity — explaining each conceptually, what breaks when it fails, and how R’s built-in diagnostic plots make checking them straightforward.

By the end of this lesson, you should be able to fit and interpret simple and multiple regression models in R, evaluate goodness of fit, test predictor significance, build a regression equation for prediction, detect and address multicollinearity, correctly include categorical variables using dummy coding, and verify that the assumptions of linear regression are reasonably satisfied using diagnostic plots and formal tests. Work through every code example in your own R script alongside the reading.

AI and Regression: From Descriptive to Predictive

This lesson marks the transition from descriptive to predictive analytics — the fourth lesson of a progression you first saw in the introductory chapter (Descriptive → Diagnostic → Predictive → Prescriptive). Regression is where that transition becomes concrete: you are no longer summarizing what happened, you are building a model to forecast what will happen.

AI accelerates every mechanical step of regression modeling. It can write lm() calls, interpret coefficient tables, check for multicollinearity, and even draft narrative interpretations of model output. The division of labor remains the same as in every earlier chapter:

| AI handles well | Requires your judgment |

|---|---|

Writing and running lm() and summary() code |

Deciding which predictors belong in the model based on theory and business logic |

| Reporting Adjusted R² and VIF scores | Evaluating whether the goodness-of-fit justifies the model’s use for prediction |

| Generating coefficient tables | Interpreting what each coefficient means in the context of your data and audience |

Applying vif() and identifying values above 5 or 10 |

Deciding whether multicollinearity is severe enough to warrant removing a predictor |

| Producing predictions from the regression equation | Determining whether predictions extrapolate dangerously beyond the training data range |

The most important AI caution for regression: a significant F-test and a high R² do not make a causal claim. AI may describe a significant predictor as “driving” or “causing” the outcome — this language is not warranted by regression analysis alone. Regression establishes that a predictor is a statistically significant linear associate of the outcome, while controlling for the other predictors in the model. Causation requires experimental design or additional theoretical justification. This distinction carries directly into how you communicate regression results to a business audience.

At a Glance

- In order to succeed at this lesson, you will use a statistical model called linear regression to understand an outcome variable and make predictions. Correlation — covered in the previous lesson — establishes whether a linear relationship exists and how strong it is. Regression uses that relationship to estimate a slope and intercept, allowing us to quantify the effect of each predictor and forecast future values. Linear regression is one of the most commonly used models in business analytics and forms the foundation for more advanced techniques like machine learning.

Lesson Objectives

- Explore the statistical model for a line.

- Compute the slope and intercept in a simple linear regression.

- Interpret regression model significance and goodness-of-fit measures (RSE, R², Adjusted R²).

- Extend to multiple regression with two or more predictors.

- Apply the p-value method for variable selection.

- Detect and interpret multicollinearity using VIF scores.

- Include categorical predictors using dummy variables.

- Identify the assumptions of linear regression, explain the consequence of each violation, and use R’s diagnostic plots and formal tests to check them.

Consider While Reading

- In this lesson, we focus on building and interpreting regression models in R. This builds on the scatterplots introduced in the Data Visualization lesson — those visualizations help us assess linearity before running a model — and on the correlation analysis from the previous lesson, which told us whether a relationship was worth modeling in the first place.

- As you read, note the connection between regression and ANOVA. The F-test in a regression output works the same way as in an ANOVA: it tests whether the variation in Y that is explained by the model is significantly greater than the unexplained variation. The sum-of-squares logic (SSR, SSE, SST) is identical.

- Pay particular attention to the distinction between the overall F-test (is the model significant?) and the individual t-tests on each coefficient (is this specific predictor significant?). In simple regression these give the same p-value, but in multiple regression they can diverge.

In the previous lesson, we used correlation to measure the strength and direction of the linear relationship between two continuous variables. Regression takes the next step: it uses that relationship to build a predictive model. Where a correlation coefficient tells you how strongly two variables move together, a regression equation tells you by how much one variable changes for each unit change in the other — and lets you forecast values you have not yet observed.

The Linear Regression Model

Overview of the Linear Regression

- Linear regression analysis is a predictive modelling technique used for building mathematical and statistical models that characterize relationships between a dependent (continuous) variable and one or more independent, or explanatory variables (continuous or categorical), all of which are numerical.

- This technique is useful in forecasting, time series modelling, and finding the causal effect between variables.

- Simple linear regression involves one explanatory variable and one response variable.

- Explanatory variable: The variable used to explain the dependent variable, usually denoted by X. Also known as an independent variable or a predictor variable.

- Response variable: The variable we wish to explain, usually denoted by Y. Also known as a dependent variable or outcome variable.

- Multiple linear regression involves two or more explanatory variables, while still only one response variable.

Examples of Independent and Dependent Variables

- Example Question: Does increasing the marketing budget lead to higher sales revenue?

- Independent Variable: Marketing budget (how much money is spent on advertising and promotions).

- Dependent Variable: Sales revenue (how much income the business generates from sales).

- Example Question: Does additional training improve employee productivity?

- Independent Variable: Hours of employee training.

- Dependent Variable: Employee productivity (e.g., units produced per hour or sales closed per month).

- Example Question: Does being a member of a loyalty program increase the frequency of repeat purchases?

- Independent Variable: Participation in a loyalty program (whether a customer is a member or not).

- Dependent Variable: Number of repeat purchases by the customer.

Estimating Using a Simple Linear Regression Model

- While the correlation coefficient may establish a linear relationship, it does not suggest that one variable causes the other.

- With regression analysis, we explicitly assume that the response variable is influenced by other explanatory variables.

- Using regression analysis, we may predict the response variable given values for our explanatory variables.

Inexact Relationships

- If the value of the response variable is uniquely determined by the values of the explanatory variables, we say that the relationship is deterministic.

- But if, as we find in most fields of research, that the relationship is inexact due to omission of relevant factors, we say that the relationship is inexact.

- In regression analysis, we include a stochastic error term, that acknowledges that the actual relationship between the response and explanatory variables is not deterministic.

Regression as ANOVA

- ANOVA conducts an F - test to determine whether variation in Y is due to varying levels of X.

- ANOVA is used to test for significance of regression:

- \(H_0\): population slope coefficient \(\beta_1\) \(=\) 0

- \(H_A\): population slope coefficient \(\beta_1\) \(\neq\) 0

- R reports the p-value (Significant F).

- Rejecting \(H_0\) indicates that X explains variation in Y.

The Simple Linear Regression Model

- The simple linear regression model is defined as \(y= \beta_0+\beta_1 𝑥+\varepsilon_1\), where \(y\) and \(x\) are the response and explanatory variables, respectively and \(\varepsilon_1\) is the random error term. \(\beta_0\) and \(\beta_1\) are the unknown parameters to be estimated.

- By fitting our data to the model, we obtain the equation \(\hat{y} = b_0 + b_1*x\), where \(\hat{y}\) is the estimated response variable, \(b_0\) is the estimate of \(\beta_0\) (Intercept) and \(b_1\) is the estimate of \(\beta_1\) (Slope).

- Sometimes, this equation can be represented using different variable names like \(y=mx+b\) This is the same equation as above, but different notation.

- Since the predictions cannot be totally accurate, the difference between the predicted and actual value represents the residual \(e=y-\hat{y}\).

The Least Squares Estimates

- The two parameters \(\beta_0\) and \(\beta_1\) are estimated by minimizing the sum of squared residuals.

- The slope coefficient \(\beta_1\) is estimated as \(b_1 = \sum(x_i-\bar{x}*y_i-\bar{y})/\sum(x_i-\bar{x})^2\)

- The intercept parameter \(\beta_0\) is estimated as \(b_0 = \hat{y}-b_1*\bar{x}\)

- And we use this information to make the regression equation given the formula above: \(\hat{y} = b_0 + b_1*x\),

Goodness of Fit

- Goodness of fit refers to how well the data fit the regression line. I will introduce three measures to judge how well the sample regression fits the data.

- Standard Error of the Estimate

- The Coefficient of Determination (\(R^2\))

- The Adjusted \(R^2\)

- In order to make sense of the goodness of fit measures, we need to go back to the idea of explained and unexplained variance we learned in the ANOVA lesson. Variance can also be known as a difference.

- Unexplained Variance = SSE or Sum of Squares Error: This equals the sum of squared difference between A and B, or between the sum of squares of the difference between observation (\(y_i\)) and our predicted value of y (\(\hat{y}\)).

- \(SSE = \sum^n_{i=1}(y_i - \hat{y})^2\)

- Explained Variance = SSR or Sum of Squares Regression: This equals the sum of squared difference between B and C, or between the sum of squares of the difference between our predicted value (\(\hat{y}\)) and the mean of y (\(\bar{y}\)).

- \(SSR = \sum^n_{i=1}(\hat{y} - \bar{y})^2\)

- Total Variance = SST or Total Sum of Squares: This equals the sum of squared difference between A and C, or between the sum of squares of the difference between observation (\(y_i\)) and the mean of y (\(\bar{y}\)).

- The SST can be broken down into two components: the variation explained by the regression equation (the regression sum of squares or SSR) and the unexplained variation (the error sum of squares or SSE).

- \(SST = \sum^n_{i=1}(y_i - \bar{y})^2\)

The Standard Error of the Estimate

- The Standard Error of the Estimate, also known as the Residual Standard Error (RSE) (and labelled such in R), is the variability between observed (\(y_i\)) and predicted (\(\hat{y}\)) values, targeting the unexplained variance in the figure above. This measure is a lack of fit of the model to the data.

- To compute the standard error of the estimate, we first compute the SSE and the MSE.

- Sum of Squares Error: \(SSE = \sum^n_{i=1}e^2_i = \sum^n_{i=1}(y_i - \hat{y})^2\)

- Dividing SSE by the appropriate degrees of freedom, n – k – 1, yields the mean squared error:

- Mean Squared Error: \(MSE = SSE/(n-k-1)\)

- The square root of the MSE is the standard error of the estimate, se.

- Standard Error of Estimate: \(se = \sqrt(MSE) = \sqrt(SSE/(n-k-1))\)

The Coefficient of Determination (\(R^2\))

Coefficient of determination refers to the percentage of variance in one variable that is accounted for by another variable or by a group of variables.

This measure of R-squared is a measure of the “fit” of the line to the data.

The Coefficient of Determination, denoted as \(R^2\), is a statistical measure that indicates the proportion of variance in the dependent variable (\(y\)) that is explained by the independent variable(s) (x) in a regression model. It is calculated as: SSR/SST or 1-SSE/SST. *\(R^2\) ranges from 0 to 1:

- \(R^2\)=0: None of the variance in \(y\) is explained by the model.

- \(R^2\)=1: The model explains all the variance in y. A higher \(R^2\) indicates a better fit of the model to the data.

\(R^2\) = 1-SSE/SST where \(SSE = \sum^n_{i=1}(y_i - \hat{y})^2\) and \(SST = \sum^n_{i=1}(y_i - \bar{y})^2\)

- \(R^2\) can also be computed by SSR/SST, which provides the same answer as above.

- This measure of fit targets both the unexplained and the explained variance.

- \(R^2\) can also be calculated using the formula for Pearson’s r and squaring it. This gives us the same answer.

Pearson’s \(r\) is a statistic that indicates the strength and direction of the relationship between two numeric variables that meet certain assumptions.

- (Pearson’s \(r\))\(^2\) = \(r^2_{xy} = (cov_{xy}/(s_x*s_y))^2\).

You need to see how all these formulas relate to see why all these formulas give you the same answer.

Interpreting (\(R^2\))

- This measure is easier to interpret over standard error. In particular, the (\(R^2\)) quantifies the fraction of variation in the response variable that is explained by changes in the explanatory variables.

- The (\(R^2\)) gives you a score between 0 and 1. A score of 1 indicates that your Y variable is perfectly explained by your X variable or variables (where we only have one in simple regression).

- The \(R^2\) measure has strength of determination like the correlation coefficient, only all measures are from 0 to 1.

- The closer you get to one, the more explained variance we achieve.

- A score of 0 indicates that no variance is explained by the X variable or variables. In this case, the variable would not be a significant predictor variable of Y.

- Again, the strength of the relationship varies by field, but generally, a .2 to a .5 is considered weak, a .5 to a .8 is considered moderate, and above a .8 is considered strong.

R Output

- We do see the \(R^2\) in our R output labelled Multiple R-squared.

Limitations of The Coefficient of Determination (\(R^2\))

- More explanatory variables always result in a higher \(R^2\).

- But some of these variables may be unimportant and should not be in the model.

- This is only applicable with multiple regression, discussed below.

The Adjusted \(R^2\)

The Adjusted Coefficient of Determination, denoted as Adjusted \(R^2\) modifies \(R^2\) to account for the number of predictors in the model relative to the number of data points. It is calculated as Adjusted \(R^2 = 1-(1-R^2)*((n-1)/(n-k-1))\), where where n is the sample size and p is the number of predictors.

In simple linear regression, \(R^2\) and Adjusted \(R^2\) will be very similar since there is only one predictor variable. The Adjusted \(R^2\) becomes more important in multiple regression, where adding more predictors can artificially inflate \(R^2\).

The Adjusted \(R^2\) tries to balance the raw explanatory power against the desire to include only important predictors.

- Adjusted \(R^2 = 1-(1-R^2)*((n-1)/(n-k-1))\).

- The Adjusted \(R^2\) penalizes the \(R^2\) for adding additional explanatory variables.

R Output

- With our other goodness-of-fit measures, we typically allow the computer to compute the Adjusted \(R^2\) using commands in R.

- Therefore, we do see the Adjusted \(R^2\) in our R output labelled Adjusted R-squared.

Example of Simple Linear Regression in R

The broad steps are the same as we used in the hypothesis testing and ANOVA modules: 1. Set up the hypothesis. 2. Compute the test statistic and calculate probability. 3. Interpret results and write a conclusion.

Step 1: Set Up the Null and Alternative Hypothesis

\(H_0\): The slope of the line is equal to zero.

\(H_A\): The slope of the line is not equal to zero.

Step 2: Compute the Test Statistic and Calculate Probability

library(tidyverse)

library(ggplot2)Debt_Payments <- read.csv("data/DebtPayments.csv")

Simple <- lm(Debt ~ Income, data = Debt_Payments)

summary(Simple)

Call:

lm(formula = Debt ~ Income, data = Debt_Payments)

Residuals:

Min 1Q Median 3Q Max

-107.087 -38.767 -5.828 50.137 101.619

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 210.298 91.339 2.302 0.0303 *

Income 10.441 1.222 8.544 9.66e-09 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 63.26 on 24 degrees of freedom

Multiple R-squared: 0.7526, Adjusted R-squared: 0.7423

F-statistic: 73 on 1 and 24 DF, p-value: 9.66e-09- Step 3: Interpret the Probability and Write a Conclusion

- We interpret the probability and write a conclusion after looking at the following:

- Goodness of Fit Measures

- The F-test statistic

- The p-value from the hypothesis

- We then can interpret the hypothesis and make the regression equation if needed to make predictions.

Examining the Goodness of Fit Measures

Like the ANOVA, we need the summary() command to see the regression output.

This output includes the following:

- Standard Error of Estimate at 63.26

- a \(R^2\) of 0.7526.

- an Adjusted \(R^2\) of 0.7423

We do not really see a difference in \(R^2\) and the Adjusted \(R^2\) because we only have a simple linear regression, which includes one X. The other thing that could create a difference between these measures is having a small sample size. A small sample size could adjust the \(R^2\) down (like it did a little here \(n=28\)). In both cases, a score around .75 indicates that we are explaining about 75% of the variance in Debt Payments, which is specifically stated as 75.26% in the \(R^2\) value.

The Standard Error of Estimate - known in R as the RSE or Residual Standard Error at 63.26.

The RSE represents the average amount by which the observed values deviate from the predicted values

The RSE has the same units as the dependent variable y, making it directly interpretable in the context of the problem.

- The scale of income is in 1000s.

- Therefore, for every 1000 dollars difference in Income we could be off on our debt payments by 63.26 dollars.

Again, most statisticians interpret the \(R^2\) and the adjusted \(R^2\) over the RSE.

Examining the F-Test Statistic

- The F-statistic is a ratio of explained information (in the numerator) to unexplained information (in the denominator). If a model explains more than it leaves unexplained, the numerator is larger and the F-statistic is greater than 1. F-statistics that are much greater than 1 are explaining much more of the variation in the outcome than they leave unexplained. Large F-statistics are more likely to be statistically significant.

- We see a F-statistic in our output with a p-value of 9.66e-09, which is less than .05. This indicates that our overall model is significant, which in simple regression means that our one X predictor variable is also significant. If this F-statistic is significant, we can interpret the hypothesis.

Examining the Hypothesis

- We see a p-value on the Income row of 9.66e-09 from a t-value. This is also significant at .05 level. This p-value is the same as the F-test statistic because we only have one X variable.

- This significance means our predictor variable does influence the Y variable and that we can reject the null hypothesis and show support for our alternative hypothesis.

- This means Income does influence Debt Payments.

Interpreting the Hypothesis

- A \(b_1\) estimate of 10.441 indicates that for 1000 dollars of Income (again our data is in 1000s), the payment of dept will increase by 10.441.

- A \(b_0\) estimate of 210.298 indicates where the regression line will start given a Y at 0.

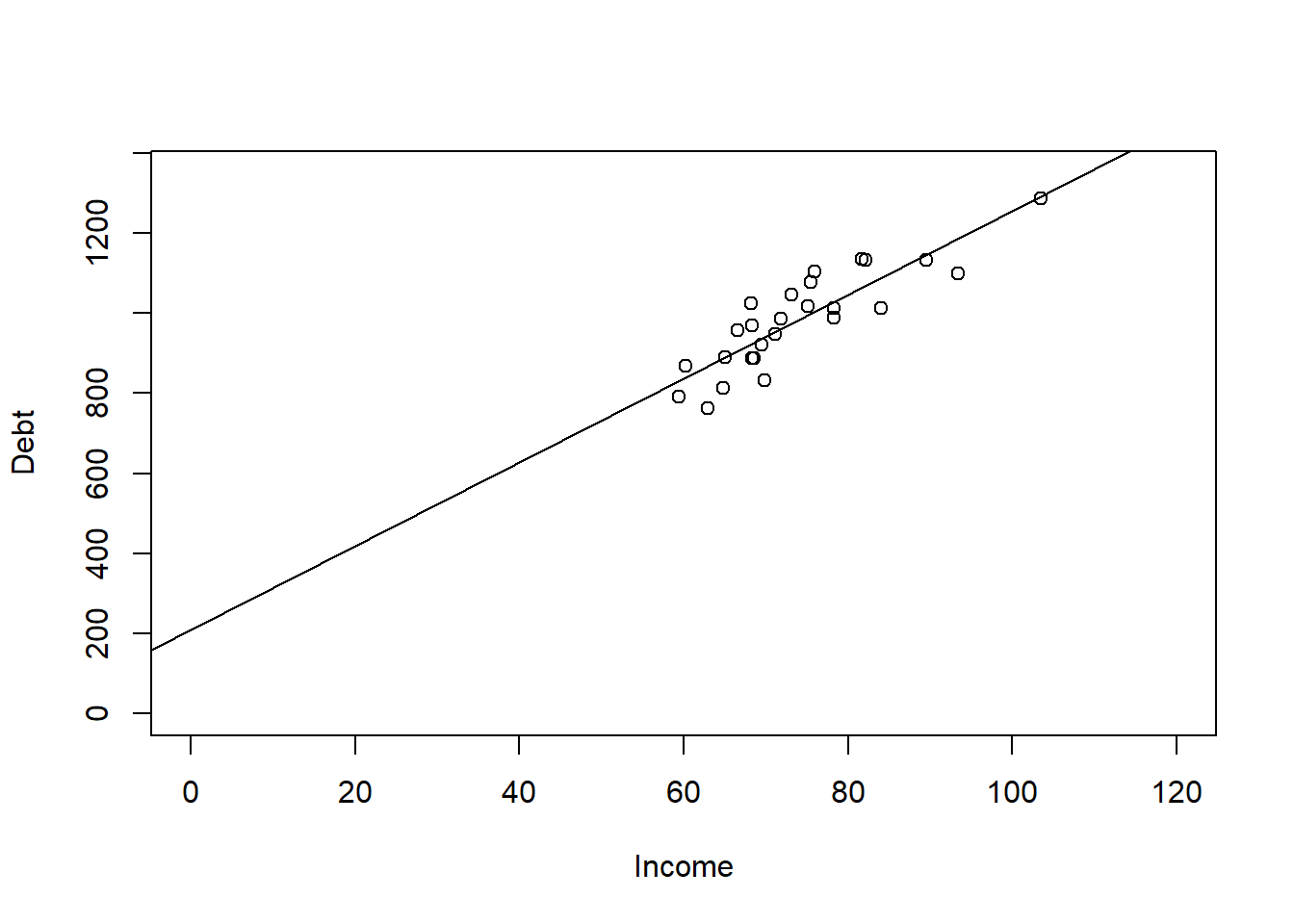

- This gives us a regression equation at \(\hat{y} = 210.298 + 10.441*Income\)

- We can graph this regression line using the abline() command on our plot we did earlier.

- As you can see from the chart, there was no data at the Y intercept, but if I extend the chart out, it does hit the y axis at 210 like stated.

- Also from the chart, we note that for each unit of income we go to the right, we go up by 10.441 units in dept payments.

plot(Debt ~ Income, data = Debt_Payments, xlim = c(0, 120), ylim = c(0,

1350))

abline(Simple)

Predictions

- We can calculate this using the regression equation or use the predict() command in order to calculate different values of y given values of x based on our regression equation we got in the step above.

- The coef() function returns the model’s coefficients which are needed to make the regression equation.

# What would be your debt payments if Income was 100 ( for 100,000)

coef(Simple)(Intercept) Income

210.29768 10.44111 210.298 + 10.441 * (100)[1] 1254.398predict(Simple, data.frame(Income = 100)) 1

1254.408 Multiple Regression

A key advantage of multiple regression over simple regression is that it allows us to control for other variables. When we include multiple predictors, each coefficient reflects the unique contribution of that variable while holding all others constant. This makes our model more realistic and our estimates more accurate — but it also means we need to be careful about which variables we include, since adding unnecessary predictors can introduce noise and obscure the relationships we care about.

Multiple regression allows us to explore how several explanatory variables influence the response variable.

Suppose there are \(k\) explanatory variables. The multiple linear regression model is defined as: \(y = \beta_0 + \beta_1x_1 + \beta_2x_2 + \ ⋯ + \beta_kx_k +\varepsilon\)

Where:

- \(y\) is the dependent variable,

- \(x_1, ⋯, x_k\) are independent explanatory variables,

- \(\beta_0\) is the intercept term,

- \(\beta_1 ⋯, \beta_k\) are the regression coefficients for the independent variables,

- \(\varepsilon\) is the random error term

We estimate the regression coefficients—called partial regression coefficients — \(b_0, b_1, b_2,… b_k\), then use the model: \(\hat{y} = b_0 + b_1x_1 + b_2x_2 + \ ... + b_kx_k\) .

The partial regression coefficients represent the expected change in the dependent variable when the associated independent variable is increased by one unit while the values of all other independent variables are held constant.

For example, if there are \(k = 3\) explanatory variables, the value \(b_1\) estimates how a change in \(x_1\) will influence \(y\) assuming \(x_2\) and \(x_3\) are held constant.

Example of Multiple Linear Regression in R

- The steps to multiple linear regression are the same as simple linear regression except we should have more than one hypothesis.

- Step 1: Set up the null and alternative hypotheses

- Hypothesis 1: Income affects Debt Payments.

- \(H_0\): The slope of the line in regards to Income is equal to zero.

- \(H_A\): The slope of the line in regards to Income is not equal to zero.

- Hypothesis 2: Unemployment affects Debt Payments.

- \(H_0\): The slope of the line in regards to Unemployment is equal to zero.

- \(H_A\): The slope of the line in regards to Unemployment is not equal to zero.

- Step 2: Compute the test statistic and calculate probability

Debt_Payments <- read.csv("data/DebtPayments.csv")

Multiple <- lm(Debt ~ Income + Unemployment, data = Debt_Payments)

summary(Multiple)

Call:

lm(formula = Debt ~ Income + Unemployment, data = Debt_Payments)

Residuals:

Min 1Q Median 3Q Max

-110.456 -38.454 -5.836 51.156 102.121

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 198.9956 156.3619 1.273 0.216

Income 10.5122 1.4765 7.120 2.98e-07 ***

Unemployment 0.6186 6.8679 0.090 0.929

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 64.61 on 23 degrees of freedom

Multiple R-squared: 0.7527, Adjusted R-squared: 0.7312

F-statistic: 35 on 2 and 23 DF, p-value: 1.054e-07- Step 3: Interpret the probability and write a conclusion

- We interpret the probability and write a conclusion after looking at the following:

- Goodness of Fit Measures

- The F-test statistic

- The p-values from the hypotheses

- We then can interpret the hypotheses and make the regression equation if needed to make predictions.

Examining the Goodness of Fit Measures

- Like the ANOVA, we need the summary() command to see the regression output.

- This output includes the following:

- Standard error of estimate at 64.61 - was previously 63.26 with simple regression.

- a \(R^2\) of 0.7527 - was previously 0.7526 with simple regression.

- an Adjusted \(R^2\) of 0.7312 - was previously 0.7423 with simple regression.

- Looking at the goodness of fit indices, they suggest that we are not explaining anything more by adding the unemployment variable over what we had with the Income variable. Our RSE and \(R^2\) are about the same, and our adjusted \(R^2\) has gone down - again paying the price for including an unnecessary variable.

Examining the F-Test Statistic

- We see a overall F-statistic in our output with a p-value of 1.054e-07, which is less than .05. This indicates that our overall model is significant - which in multiple regression means that at least one X predictor variable is significant. If this F-statistic is significant, we can interpret the hypotheses.

Examining the Hypotheses

- Hypothesis 1: The output shows a p-value on the Income row of 2.98e-07 from a t-value. This was significant in our simple regression model, and is still significant at .05 level here. This significance means our predictor variable does influence the Y variable and that we can reject the null hypothesis and show support for our alternative hypothesis.

- Hypothesis 2: The output shows a p-value on the Unemployment row of 0.929 from a t-value. This is NOT significant at any appropriate level of alpha. This lack of significance means our predictor variable does NOT influence the Y variable and that we fail to reject the null hypothesis that there is a slope.

Interpreting the Hypothesis

- Because Unemployment is not significant, we should drop it from the model before creating the regression equation. The extra variable is only adding noise to our model and not adding anything useful in understanding debt payments.

The P-value Method

When you have a lot of predictors, it can be difficult to come up with a good model.

A common criteria is to remove based on the highest p-value.

Remove indicators until all variables are significant, and none are insignificant.

As we drop variables, we also want to keep an eye on the adjusted R-Squared to make sure it does not significantly decrease. It should stay about the same if we drop variables that are not helpful in understanding the model, and could improve because we are decreasing the number of variables being evaluated.

library(ISLR)

data("Credit")

str(Credit)'data.frame': 400 obs. of 12 variables:

$ ID : int 1 2 3 4 5 6 7 8 9 10 ...

$ Income : num 14.9 106 104.6 148.9 55.9 ...

$ Limit : int 3606 6645 7075 9504 4897 8047 3388 7114 3300 6819 ...

$ Rating : int 283 483 514 681 357 569 259 512 266 491 ...

$ Cards : int 2 3 4 3 2 4 2 2 5 3 ...

$ Age : int 34 82 71 36 68 77 37 87 66 41 ...

$ Education: int 11 15 11 11 16 10 12 9 13 19 ...

$ Gender : Factor w/ 2 levels " Male","Female": 1 2 1 2 1 1 2 1 2 2 ...

$ Student : Factor w/ 2 levels "No","Yes": 1 2 1 1 1 1 1 1 1 2 ...

$ Married : Factor w/ 2 levels "No","Yes": 2 2 1 1 2 1 1 1 1 2 ...

$ Ethnicity: Factor w/ 3 levels "African American",..: 3 2 2 2 3 3 1 2 3 1 ...

$ Balance : int 333 903 580 964 331 1151 203 872 279 1350 ...library(tidyverse)

## Removing variables that are of no interest to the model based on

## what we have learned so far. The following lines removes the

## categorical variables, Gender, Student, Married, and Ethnicity. It

## also removed the ID because that is not a helpful variable.

Credit <- select(Credit, -Gender, -Student, -Married, -Ethnicity, -ID)

creditlm <- lm(Balance ~ ., data = Credit)

summary(creditlm)

Call:

lm(formula = Balance ~ ., data = Credit)

Residuals:

Min 1Q Median 3Q Max

-227.25 -113.15 -42.06 45.82 542.97

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -477.95809 55.06529 -8.680 < 2e-16 ***

Income -7.55804 0.38237 -19.766 < 2e-16 ***

Limit 0.12585 0.05304 2.373 0.01813 *

Rating 2.06310 0.79426 2.598 0.00974 **

Cards 11.59156 7.06670 1.640 0.10174

Age -0.89240 0.47808 -1.867 0.06270 .

Education 1.99828 2.59979 0.769 0.44257

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 161.6 on 393 degrees of freedom

Multiple R-squared: 0.8782, Adjusted R-squared: 0.8764

F-statistic: 472.5 on 6 and 393 DF, p-value: < 2.2e-16# Multiple R-squared: 0.8782, Adjusted R-squared: 0.8764- Education has the highest p-value, so it is removed from analysis. We use the minus sign to remove the variable in the lm function.

creditlm <- lm(Balance ~ . - Education, data = Credit)

summary(creditlm)

Call:

lm(formula = Balance ~ . - Education, data = Credit)

Residuals:

Min 1Q Median 3Q Max

-231.37 -113.46 -39.55 41.66 544.35

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -449.36101 40.57409 -11.075 <2e-16 ***

Income -7.56211 0.38214 -19.789 <2e-16 ***

Limit 0.12855 0.05289 2.430 0.0155 *

Rating 2.02240 0.79208 2.553 0.0110 *

Cards 11.55272 7.06285 1.636 0.1027

Age -0.88832 0.47781 -1.859 0.0638 .

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 161.6 on 394 degrees of freedom

Multiple R-squared: 0.8781, Adjusted R-squared: 0.8765

F-statistic: 567.4 on 5 and 394 DF, p-value: < 2.2e-16# Multiple R-squared: 0.8781, Adjusted R-squared: 0.8765- Cards has the next highest p-value, so it is removed from analysis using the - minus sign format.

creditlm <- lm(Balance ~ . - Education - Cards, data = Credit)

summary(creditlm)

Call:

lm(formula = Balance ~ . - Education - Cards, data = Credit)

Residuals:

Min 1Q Median 3Q Max

-249.62 -110.89 -39.98 51.87 546.52

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -445.10477 40.57635 -10.970 < 2e-16 ***

Income -7.61268 0.38169 -19.945 < 2e-16 ***

Limit 0.08183 0.04461 1.834 0.0674 .

Rating 2.73142 0.66435 4.111 4.79e-05 ***

Age -0.85612 0.47841 -1.789 0.0743 .

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 161.9 on 395 degrees of freedom

Multiple R-squared: 0.8772, Adjusted R-squared: 0.876

F-statistic: 705.6 on 4 and 395 DF, p-value: < 2.2e-16# Multiple R-squared: 0.8772, Adjusted R-squared: 0.876- Age is next to be removed because it has the next highest p-value at .06270.

creditlm <- lm(Balance ~ . - Education - Cards - Age, data = Credit)

summary(creditlm)

Call:

lm(formula = Balance ~ . - Education - Cards - Age, data = Credit)

Residuals:

Min 1Q Median 3Q Max

-260.93 -113.14 -36.27 49.35 554.23

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -489.72748 32.09892 -15.257 < 2e-16 ***

Income -7.71931 0.37806 -20.418 < 2e-16 ***

Limit 0.08467 0.04471 1.894 0.059 .

Rating 2.69858 0.66594 4.052 6.11e-05 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 162.4 on 396 degrees of freedom

Multiple R-squared: 0.8762, Adjusted R-squared: 0.8753

F-statistic: 934.6 on 3 and 396 DF, p-value: < 2.2e-16# Multiple R-squared: 0.8762, Adjusted R-squared: 0.8753Finally Limit is the next to be removed because it has the next highest (and still insignificant) p-value at .059.

Age is next to be removed because it has the next highest p-value at .06270.

creditlm <- lm(Balance ~ . - Education - Cards - Age - Limit, data = Credit)

summary(creditlm)

Call:

lm(formula = Balance ~ . - Education - Cards - Age - Limit, data = Credit)

Residuals:

Min 1Q Median 3Q Max

-278.57 -112.69 -36.21 57.92 575.24

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -534.81215 21.60270 -24.76 <2e-16 ***

Income -7.67212 0.37846 -20.27 <2e-16 ***

Rating 3.94926 0.08621 45.81 <2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 162.9 on 397 degrees of freedom

Multiple R-squared: 0.8751, Adjusted R-squared: 0.8745

F-statistic: 1391 on 2 and 397 DF, p-value: < 2.2e-16# Multiple R-squared: 0.8751,Adjusted R-squared: 0.8745- In our original model with non-helpful insignificant predictors, we had an adjusted R-Squared at 0.8764. After removing insignificant predictors, we are only down to .8745. This means we can explain someones Balance best by understanding Income and Rating.

- The interpretation is as follows:

- A one unit change in Income causes a negative 7.67 change in Balance.

- A one unit change in Rating causes a 3.949 change in Balance.

Multicollinerity

- Multicollinearity refers to the situation in which two or more predictor variables are closely related to another.

- Collinearity can cause significant factors to be insignificant, or insignificant factors to seem significant. Both are problematic.

- If sample correlation coefficient between 2 explanatory variables is more than .80 or less than -.80, we could have severe multicollinearity. Seemingly wrong signs of estimated regression coefficients may also indicate multicollinearity. A good remedy may be to simply drop one of the collinear variables if we can justify it as redundant.

- Alternatively, we could try to increase our sample size.

- Another option would be to try to transform our variables so that they are no longer collinear.

- Last, especially if we are interested only in maintaining a high predictive power, it may make sense to do nothing.

cor(Credit$Income, Credit$Rating) ##close to .8, but still under[1] 0.7913776- The second way to tell if there is multicollinearity is to use the vif() command from the car package.

- The vif() function in R is used to calculate the Variance Inflation Factor (VIF) for each predictor variable in a multiple regression model. The VIF quantifies how much the variance of a regression coefficient is inflated due to multicollinearity among the predictors. High VIF values indicate high multicollinearity, which can affect the stability and interpretability of the regression coefficients.

- We want all scores to be under 10 to indicate the absence of problematic multicollinerity in our model.

library(car) ##need to have car package installed first.

# Place regression model object in the function to see vif scores.

vif(creditlm) Income Rating

2.67579 2.67579 - While statisticians differ on what constitutes, the general consensus is that scores need to be under 5 or 10.

- Both scores are under 10, so we do have an absence of multicollinerity in our final model.

- VIF = 1: No correlation between the predictor and the other predictors.

- 1 < VIF < 5: Moderate correlation but not severe enough to require correction. Scores less than 5 pass assumption.

- 5 < VIF < 10: High correlation, indicating potential multicollinearity problems. We keep an eye on this issue, but pass the assumption.

- VIF >= 10: High correlation, indicating multicollinearity problems. Fail assumption.

Regression with Categorical Variables

Simple and multiple regression both require a continuous dependent variable (y). However, the predictor variables (x) can be categorical or continuous. If you were to have a y/x pairing with a continuous y and a categorical x, you might as well choose to run an ANOVA from the last module or a t-test if there are only 2 categories. However, if you have a more complex model, or need to try a variety of models, multiple regression allows for you to seamlessly add and delete predictor variables (both categorical and continuous).

We often have categorical predictors in modeling settings. And it might not make sense to think about a “one unit increase” in a categorical variable. In regression settings, we can account for categorical variables by creating dummy variables, which are indicator variables for certain conditions happening. When considering categorical variables, one variable is taken to be the baseline or reference value. All other categories will be compared to it.

Regression analysis requires numerical data.

Ordinal variables can be represented by a number in one column when there is even distance between the categories.

- From strongly disagree to disagree to N/A to agree to strongly agree. Each 1 unit change considers the same distance between points.

- A weighted scale would go from strongly disagree to neither to agree to strongly agree to agree all the time.

- Need to manually code these and coerce into a number.

- Some ordinal variables need to use dummy coding in R (i.e., Seasonality). Need to always check rationale before blindly recoding to numbers, or using numbers that were provided.

Nominal categorical data can be included as independent variables, but must be coded numeric using dummy variables.

- R will create the dummy variables automatically in a regression using the lm() command.

- For variables with 2 categories, code as 0 and 1.

Dummy Variables with More than 2 Categories

- Like in an ANOVA test, a categorical variable may be defined by more than two categories.

- Use multiple dummy variables to capture all categories, one for each category.

- When a categorical variable has k > 2 levels, we need to add k − 1 additional variables to the model.

- Given the intercept term, we exclude one of the dummy variables from the regression.

- The excluded variable represents the reference category.

- Including all dummy variables creates perfect multicollinearity (which is an assumption discussed in your textbook).

- Example: mode of transportation with three categories

- Public transportation, driving alone, or car pooling

- \(d_1=1\) for public transportation and 0 otherwise

- \(d_2=1\) for driving alone and 0 otherwise

- \(d_1=d_2=0\) indicates car pooling

- Public transportation, driving alone, or car pooling

- Slope estimates of categorical data cannot be evaluated the same way. In the example below, since Gender is nominal, and because we are using regression, we should use dummy variables to process this factor in the regression instead of the method above. We can use this technique for ordinal variables to recode them into numeric. Again, R does this coding on our behalf using the lm() command.

# Take a vector representing gender

gender <- c("MALE", "FEMALE", "FEMALE", "UNKNOWN", "MALE")

# One way is to convert the data into numerical in the column using

# ifelse statements.

ifelse(gender == "MALE", 1, ifelse(gender == "FEMALE", 2, 99))[1] 1 2 2 99 1Example Using Dummy Variables

- Suppose that we are forecasting and we want to account for the month as a predictor.

- Then the following dummy variables can be created the following way:

sales <- read.csv("data/months.csv", stringsAsFactors = TRUE)

str(sales)'data.frame': 132 obs. of 3 variables:

$ Month: Factor w/ 12 levels "Apr","Aug","Dec",..: 1 2 3 4 5 6 7 8 9 10 ...

$ Year : int 2010 2010 2010 2010 2010 2010 2010 2010 2010 2010 ...

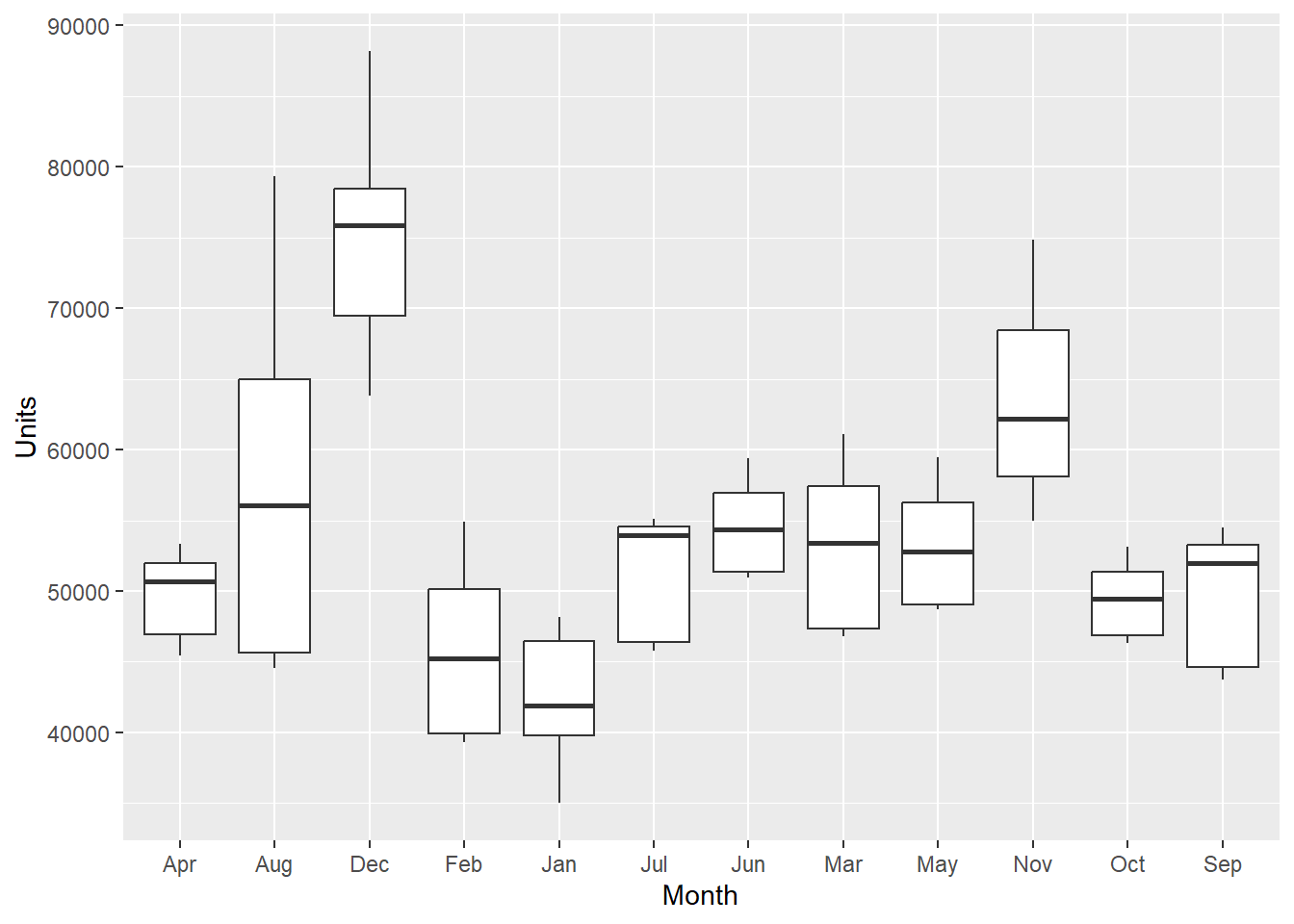

$ Units: int 45420 44558 63844 39338 35000 45747 50923 46786 48696 55000 ...library(tidyverse)ggplot(sales, aes(x = Month, y = Units)) + geom_boxplot()

- I produced a boxplot of the monthly data across units above. April (Apr) is the first month listed (not Jan for January). It alphabetizes it from there from left to right.

- Looking at the lm() command summary below, the hypotheses take on the format VariableCategory. So MonthAug corresponds to the Month variable with the Aug category, representing August. You will notice that there is no MonthApr listed. It is considered the referent category and held in the intercept.

- The interpretation of each of the coefficients associated with the dummy variables is that it is a measure of the effect of that category relative to the omitted or referent category.

- In the example to the left, the intercept coefficient is associated with April, so MonthAug measures the effect of August on the forecast variable (Units) compared to the effect of April.

- Since the data represents the difference in Units sold in months, we can interpret the predicted units sold for April as 49,580.8.

- August was significantly different than April because there is a p-value less than .05. Specifically, we can expect about 7701.6 more units to be sold in August over April. December, January, June, and November also had significantly different Units sold.

- February, July, March, May, October, and September are not different than April because the p-value is > .05.

- Never try to remove a categorical variable that is not significant because it means something else - that the category is not different than the referent category. More on this later.

# Suppose that we are forecasting daily data and we want to account

# for the month as a predictor. Then the following dummy variables

# can be created.

lmSales <- lm(Units ~ Month, data = sales)

summary(lmSales)

Call:

lm(formula = Units ~ Month, data = sales)

Residuals:

Min 1Q Median 3Q Max

-12724.5 -4056.6 -36.3 3620.9 22066.5

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 49580.8 1749.6 28.339 < 2e-16 ***

MonthAug 7701.6 2474.2 3.113 0.00232 **

MonthDec 25245.7 2474.2 10.203 < 2e-16 ***

MonthFeb -3744.7 2474.2 -1.513 0.13279

MonthJan -6939.5 2474.2 -2.805 0.00588 **

MonthJul 1809.8 2474.2 0.731 0.46592

MonthJun 4971.5 2474.2 2.009 0.04675 *

MonthMar 3671.9 2474.2 1.484 0.14042

MonthMay 3652.1 2474.2 1.476 0.14255

MonthNov 14205.6 2474.2 5.741 7.21e-08 ***

MonthOct -125.4 2474.2 -0.051 0.95967

MonthSep 261.8 2474.2 0.106 0.91590

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 5803 on 120 degrees of freedom

Multiple R-squared: 0.6857, Adjusted R-squared: 0.6569

F-statistic: 23.8 on 11 and 120 DF, p-value: < 2.2e-16# The Intercept absorbs the referent category and so in this case,

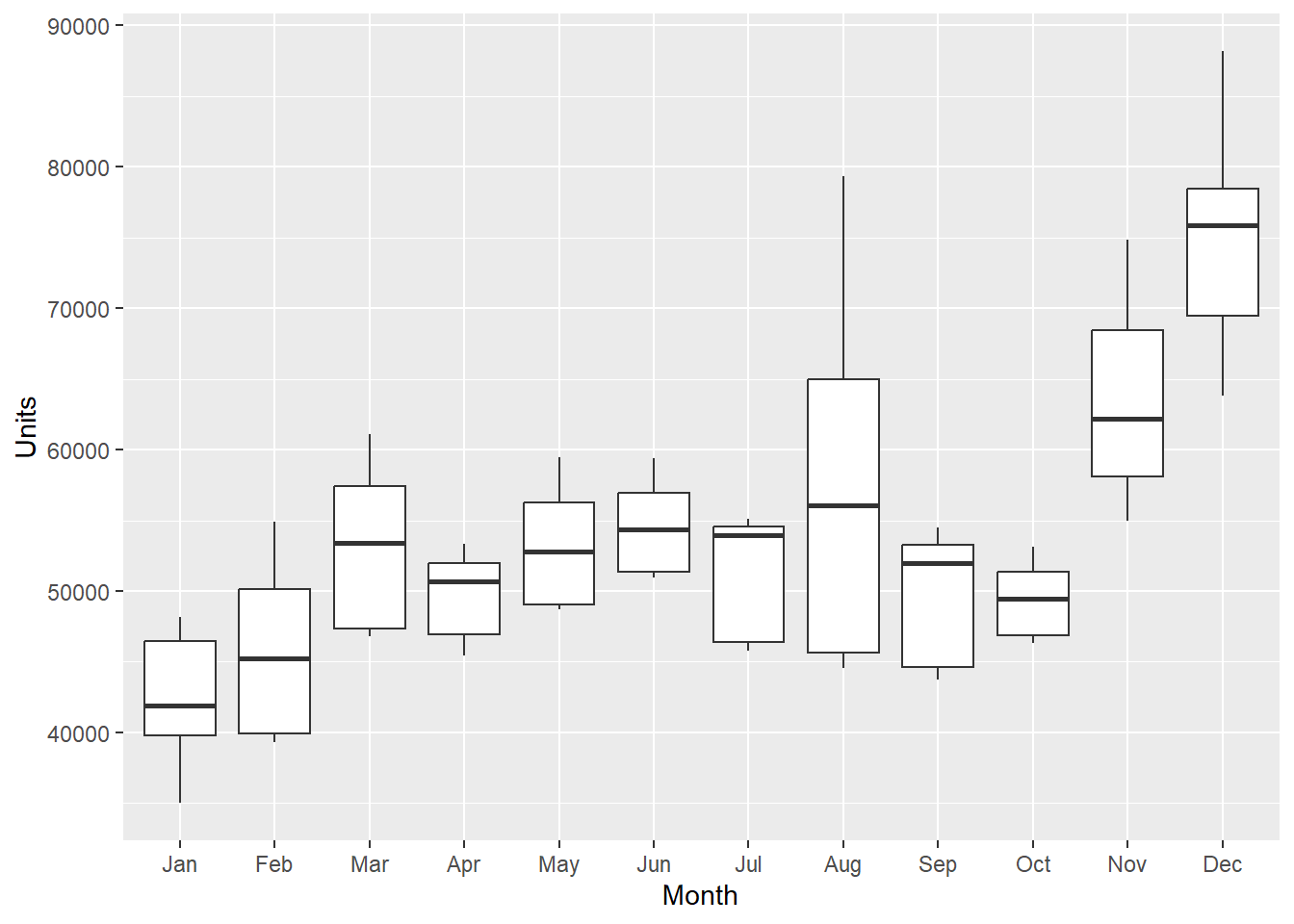

# April is alphabetically first and the referent category.- We can reset the levels by using the factor() command. Shown below, I reset the levels of the month in order from month 1 (Jan) to month 12 (Dec). This puts “Jan” in the referent category when we rerun the regression. This allows us to compare Jan to other months and to specifically, test what months are different from Jan (+ increase in sales from Jan, - a decrease in sales from Jan).

- For example, March has 10612 more unit sales than Jan. If not significant, like MonthFeb, then you can interpret as not significantly different than the 42K in Jan.

sales$Month <- factor(sales$Month, levels = c("Jan", "Feb", "Mar", "Apr",

"May", "Jun", "Jul", "Aug", "Sep", "Oct", "Nov", "Dec"))

ggplot(sales, aes(x = Month, y = Units)) + geom_boxplot()

lmSales <- lm(Units ~ Month, data = sales)

summary(lmSales)

Call:

lm(formula = Units ~ Month, data = sales)

Residuals:

Min 1Q Median 3Q Max

-12724.5 -4056.6 -36.3 3620.9 22066.5

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 42641 1750 24.373 < 2e-16 ***

MonthFeb 3195 2474 1.291 0.199106

MonthMar 10612 2474 4.289 3.65e-05 ***

MonthApr 6940 2474 2.805 0.005877 **

MonthMay 10592 2474 4.281 3.77e-05 ***

MonthJun 11911 2474 4.814 4.36e-06 ***

MonthJul 8749 2474 3.536 0.000578 ***

MonthAug 14641 2474 5.917 3.17e-08 ***

MonthSep 7201 2474 2.911 0.004302 **

MonthOct 6814 2474 2.754 0.006803 **

MonthNov 21145 2474 8.546 4.78e-14 ***

MonthDec 32185 2474 13.008 < 2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 5803 on 120 degrees of freedom

Multiple R-squared: 0.6857, Adjusted R-squared: 0.6569

F-statistic: 23.8 on 11 and 120 DF, p-value: < 2.2e-16# The interpretation of each of the coefficients associated with the

# dummy variables is that it is a measure of the effect of that

# category relative to the omitted category. In the example to the

# left, the intercept coefficient is associated with January, so

# MonthFeb measures the effect of Feb on the forecast variable

# (Units) compared to the effect of Jan.Example Using a Continuous and Categorical Variable

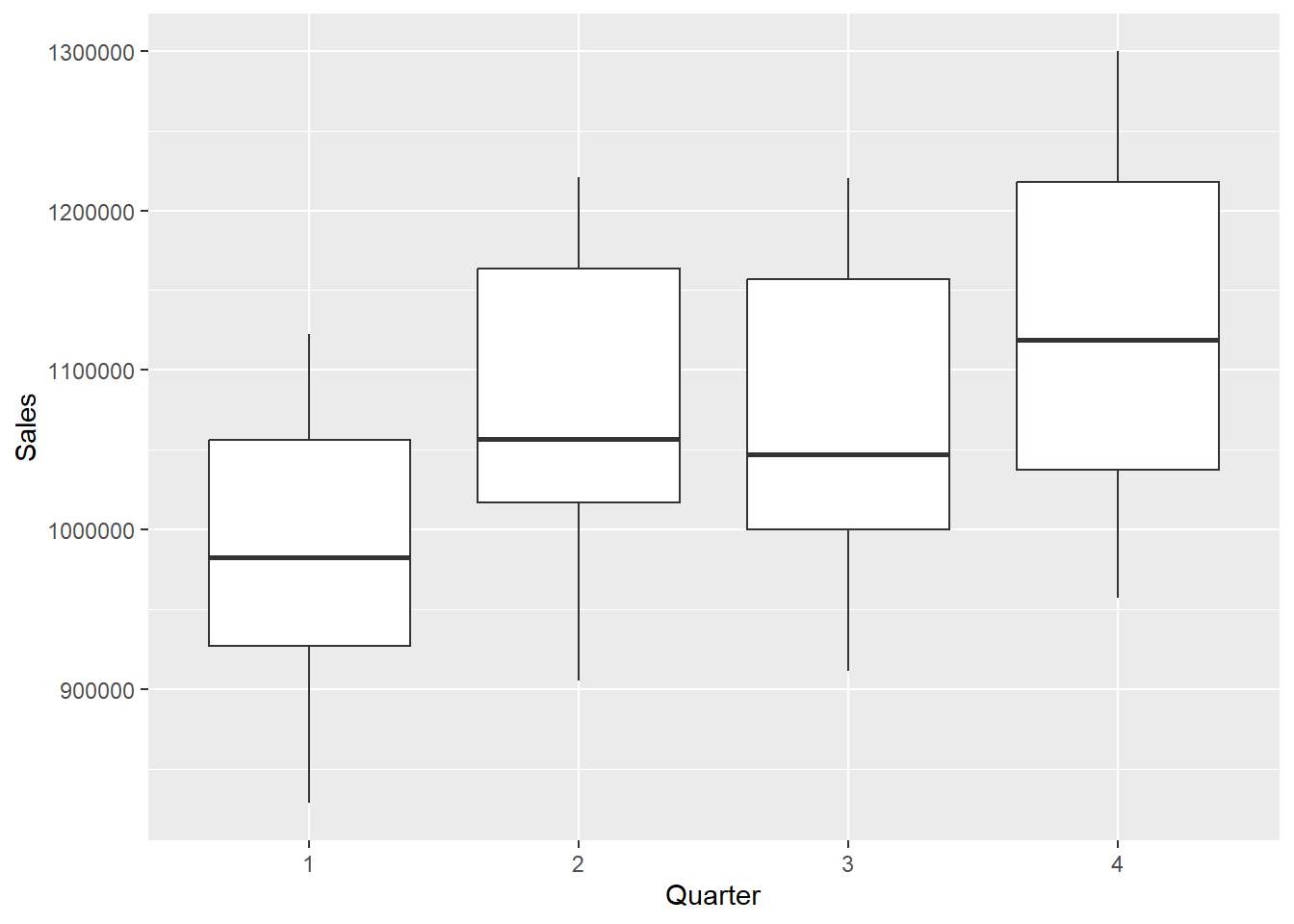

- Let’s do an example with the GNP.csv data set to use GNP and quarterly data to predict Sales (in millions)

GNP <- read.csv("data/GNP.csv")

str(GNP)'data.frame': 40 obs. of 4 variables:

$ Year : int 2007 2007 2007 2007 2008 2008 2008 2008 2009 2009 ...

$ Quarter: int 1 2 3 4 1 2 3 4 1 2 ...

$ Sales : int 921266 1013371 1000151 1060394 950268 1028016 999824 957207 828677 905562 ...

$ GNP : num 14302 14513 14718 14880 14849 ...# #1, 2, 3, 4 represent the quarter and we want that data as

# categorical

GNP$Quarter <- as.factor(GNP$Quarter)

# #Evaluate Quarterly data of GNP in a boxplot.

GNP %>%

ggplot(aes(x = Quarter, y = Sales)) + geom_boxplot()

# Run the linear regression considering GNP and Quarterly data

lmGNP <- lm(Sales ~ GNP + Quarter, data = GNP)

summary(lmGNP)

Call:

lm(formula = Sales ~ GNP + Quarter, data = GNP)

Residuals:

Min 1Q Median 3Q Max

-53748 -20083 -700 16341 52626

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -61669.572 52583.805 -1.173 0.249

GNP 65.055 3.215 20.234 < 2e-16 ***

Quarter2 78278.963 13576.443 5.766 1.57e-06 ***

Quarter3 59960.212 13607.096 4.407 9.49e-05 ***

Quarter4 108765.258 13638.197 7.975 2.21e-09 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 30330 on 35 degrees of freedom

Multiple R-squared: 0.9364, Adjusted R-squared: 0.9291

F-statistic: 128.7 on 4 and 35 DF, p-value: < 2.2e-16# Estimate y, where y and x are Sales and GNP, and 2 is a quarter 2

# dummy, 3 is a Quarter 3 dummy, and 4 is a Quarter 4 dummy.

# All else equal, retail sales in quarter 1 are expected to be

# approximately $108,765 million less than sales in quarter 4.

# What are the predicted sales in quarter 2 if GNP is $18,000 (in

# billions)?

Quarter2 <- 18000

coef(lmGNP) (Intercept) GNP Quarter2 Quarter3 Quarter4

-61669.57208 65.05476 78278.96330 59960.21187 108765.25801 # Using the equation

-61669.57208 + 65.05476 * Quarter2 + 78278.963[1] 1187595# When you use the predict() command with a categorical variable, you

# need to include the predictors with what they equal as shown below.

# I pulled out the data.frame() command into a new variable named nd

# to simplify our predict() command later on.

nd <- data.frame(GNP = 18000, Quarter = "2")

predict(lmGNP, nd) 1

1187595 # You can write the above 2 lines like shown below for the same

# answer.

predict(lmGNP, data.frame(GNP = 18000, Quarter = "2")) 1

1187595 - While you technically can keep adding categorical variables, you must be careful not to add too many because the intercept becomes increasingly difficult to interpret!

Coffee Example

Visualizing

- Let’s try a bigger example with the coffee dataset.

library(tidyverse)

library(ggplot2)

library(dplyr)

coffee <- read.csv("data/coffee.csv", stringsAsFactors = TRUE)

str(coffee)'data.frame': 1311 obs. of 31 variables:

$ X : int 1 2 3 4 5 6 7 8 9 10 ...

$ Species : Factor w/ 1 level "Arabica": 1 1 1 1 1 1 1 1 1 1 ...

$ Owner : Factor w/ 306 levels "","acacia hills ltd",..: 206 206 125 302 206 154 137 95 95 75 ...

$ Country.of.Origin : Factor w/ 37 levels "","Brazil","Burundi",..: 10 10 11 10 10 2 26 10 10 10 ...

$ Farm.Name : Factor w/ 558 levels "","-","1","200 farms",..: 374 374 441 526 374 1 1 19 19 510 ...

$ ICO.Number : Factor w/ 843 levels "","-","??","0",..: 455 455 1 1 455 1 1 98 98 454 ...

$ Company : Factor w/ 271 levels "","ac la laja sa de cv",..: 169 169 1 264 169 1 208 1 1 88 ...

$ Number.of.Bags : int 300 300 5 320 300 100 100 300 300 50 ...

$ Bag.Weight : Factor w/ 56 levels "0 kg","0 lbs",..: 47 47 3 47 47 32 51 47 47 47 ...

$ Harvest.Year : Factor w/ 47 levels "","08/09 crop",..: 16 16 1 16 16 14 13 41 41 16 ...

$ Processing.Method : Factor w/ 6 levels "","Natural / Dry",..: 6 6 1 2 6 2 6 1 1 2 ...

$ Color : Factor w/ 5 levels "","Blue-Green",..: 4 4 1 4 4 3 3 1 1 4 ...

$ Aroma : num 8.67 8.75 8.42 8.17 8.25 8.58 8.42 8.25 8.67 8.08 ...

$ Flavor : num 8.83 8.67 8.5 8.58 8.5 8.42 8.5 8.33 8.67 8.58 ...

$ Aftertaste : num 8.67 8.5 8.42 8.42 8.25 8.42 8.33 8.5 8.58 8.5 ...

$ Acidity : num 8.75 8.58 8.42 8.42 8.5 8.5 8.5 8.42 8.42 8.5 ...

$ Body : num 8.5 8.42 8.33 8.5 8.42 8.25 8.25 8.33 8.33 7.67 ...

$ Balance : num 8.42 8.42 8.42 8.25 8.33 8.33 8.25 8.5 8.42 8.42 ...

$ Uniformity : num 10 10 10 10 10 10 10 10 9.33 10 ...

$ Clean.Cup : num 10 10 10 10 10 10 10 10 10 10 ...

$ Sweetness : num 10 10 10 10 10 10 10 9.33 9.33 10 ...

$ Cupper.Points : num 8.75 8.58 9.25 8.67 8.58 8.33 8.5 9 8.67 8.5 ...

$ Moisture : num 0.12 0.12 0 0.11 0.12 0.11 0.11 0.03 0.03 0.1 ...

$ Category.One.Defects: int 0 0 0 0 0 0 0 0 0 0 ...

$ Quakers : int 0 0 0 0 0 0 0 0 0 0 ...

$ Category.Two.Defects: int 0 1 0 2 2 1 0 0 0 4 ...

$ unit_of_measurement : Factor w/ 2 levels "ft","m": 2 2 2 2 2 2 2 2 2 2 ...

$ altitude_low_meters : num 1950 1950 1600 1800 1950 ...

$ altitude_high_meters: num 2200 2200 1800 2200 2200 NA NA 1700 1700 1850 ...

$ altitude_mean_meters: num 2075 2075 1700 2000 2075 ...

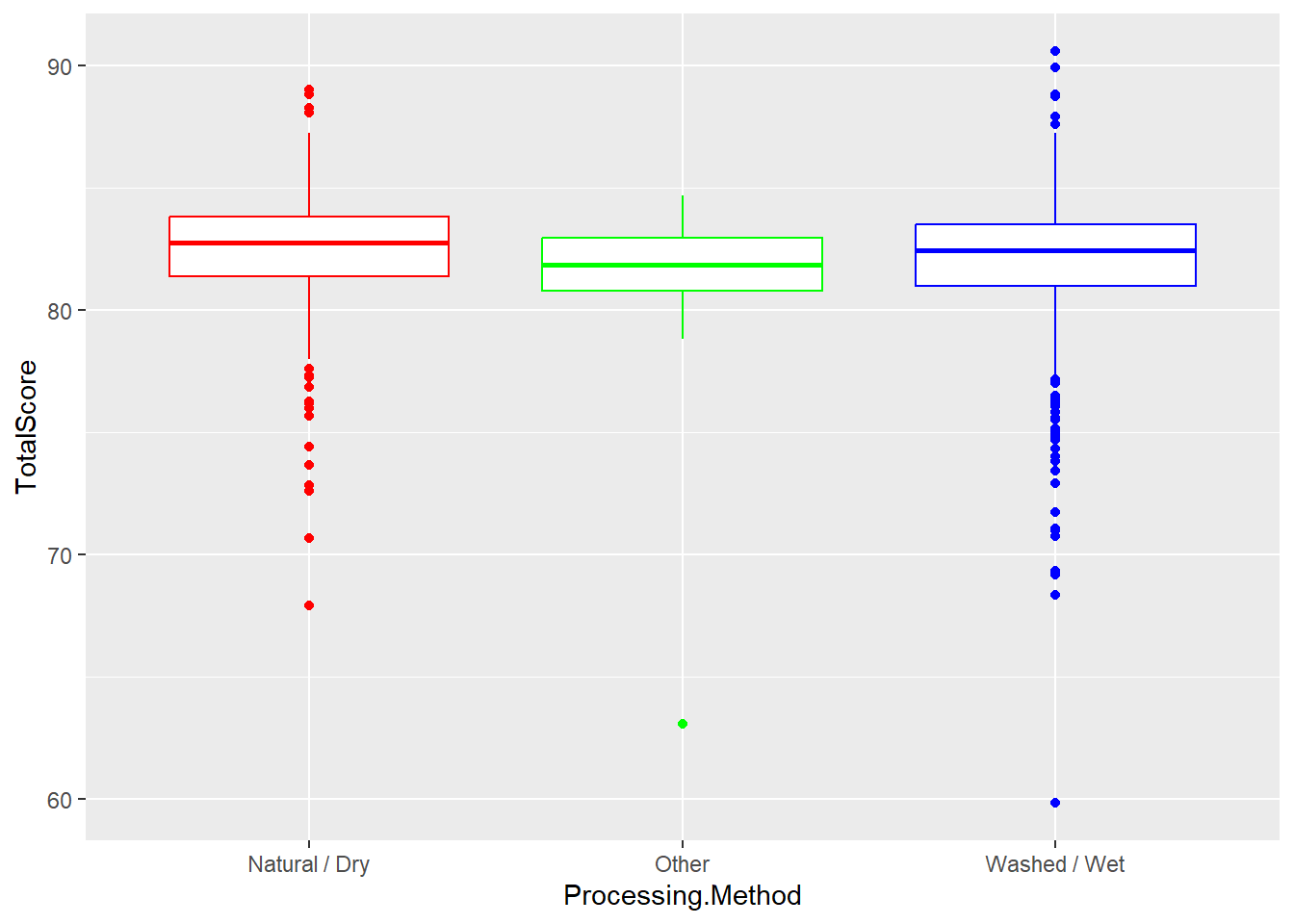

$ TotalScore : num 90.6 89.9 89.8 89 88.8 ...- Sometimes, we are only interested in 2 or 3 category values. In the following example, I am filtering by Processing Method and creating a ggplot only holding the methods of interest to me.

coffee %>%

filter(Processing.Method == "Natural / Dry" | Processing.Method ==

"Washed / Wet" | Processing.Method == "Other") %>%

ggplot(aes(x = Processing.Method, y = TotalScore)) + geom_boxplot(color = rainbow(3))

- Does not look like large group differences, good indication into what we will find.

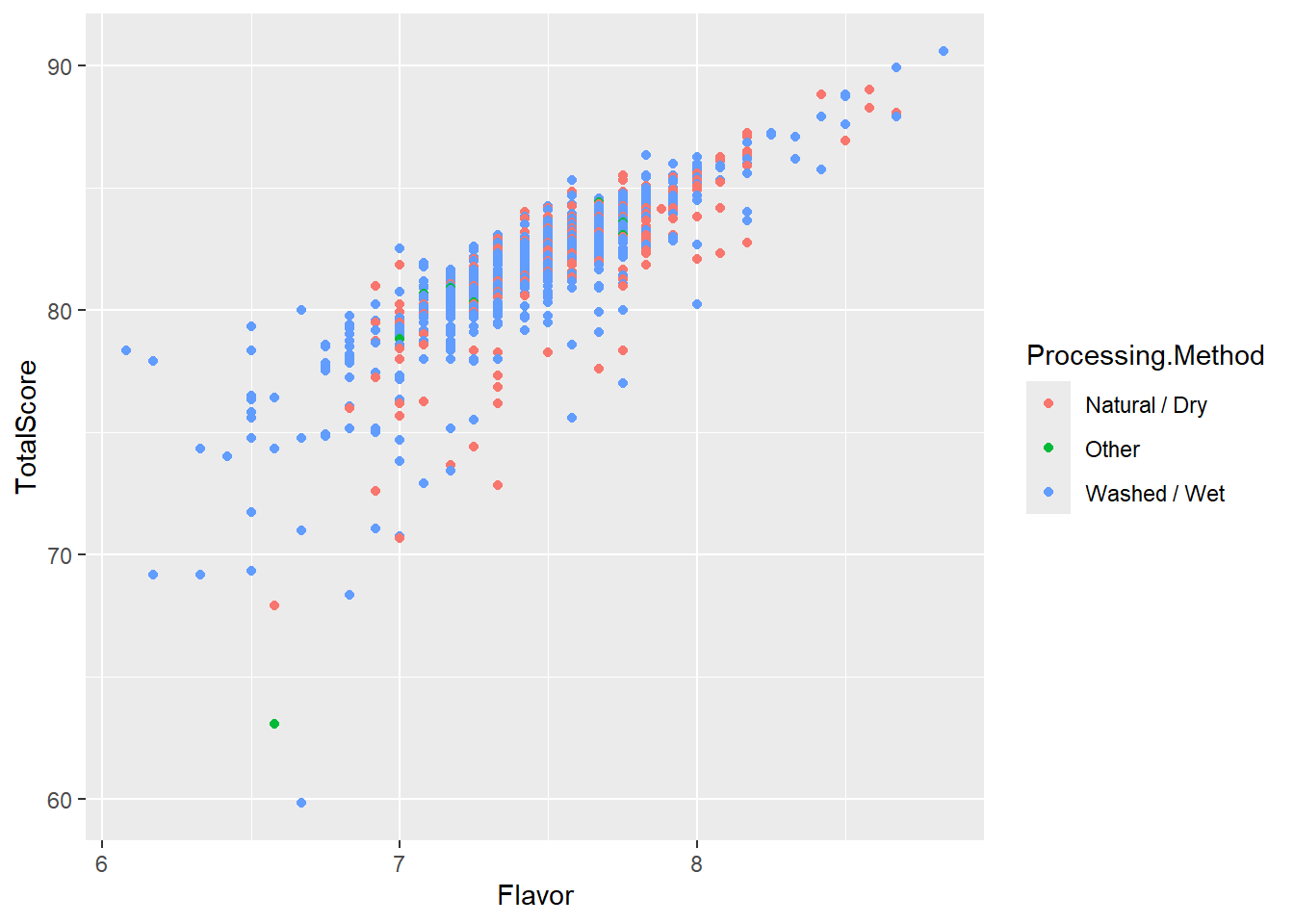

- In the next visualization, lets add in a scatterplot to show the difference between 2 continuous variables (Flavor and TotalScore) using Processing Method method as the color.

coffee %>%

filter(Processing.Method == "Natural / Dry" | Processing.Method ==

"Washed / Wet" | Processing.Method == "Other") %>%

ggplot(aes(x = Flavor, y = TotalScore, color = Processing.Method)) +

geom_point(aes(fill = Processing.Method))

- In the chart above, flavor almost looks like a perfect predictor, strong and positive.

2 Categories

- Suppose there are only 2 processing methods for coffee beans: Wet/Washed and Natural/Dry.

R takes Natural/Dry as the referent category value. Then we can create one dummy variable. A Dummy Variable is then assigned as either a 0 or 1. Let’s save the filtering of 2 methods into a new smaller dataset first and then running the lm model.

coffee2cat <- filter(coffee, Processing.Method == "Natural / Dry" | Processing.Method ==

"Washed / Wet")

head(coffee2cat$Processing.Method)[1] Washed / Wet Washed / Wet Natural / Dry Washed / Wet Natural / Dry

[6] Washed / Wet

6 Levels: Natural / Dry Other ... Washed / Wet- Next, lets run a lm model using the newly filtered data.

lmModel <- lm(TotalScore ~ Processing.Method, data = coffee2cat)

summary(lmModel)

Call:

lm(formula = TotalScore ~ Processing.Method, data = coffee2cat)

Residuals:

Min 1Q Median 3Q Max

-22.1346 -0.9944 0.4554 1.5354 8.6154

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 82.3541 0.1704 483.193 <2e-16 ***

Processing.MethodWashed / Wet -0.3895 0.1950 -1.997 0.046 *

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 2.7 on 1061 degrees of freedom

Multiple R-squared: 0.003746, Adjusted R-squared: 0.002807

F-statistic: 3.99 on 1 and 1061 DF, p-value: 0.04603- We can make a prediction of Washed/Wet.

predict(lmModel, data.frame(Processing.Method = "Washed / Wet")) 1

81.96462 coef(lmModel) (Intercept) Processing.MethodWashed / Wet

82.3541434 -0.3895252 82.3541 - 0.3895[1] 81.9646Using More Than 2 Categories

A categorical variable may be defined by more than two categories.

Like mentioned above, we use multiple dummy variables to capture all categories, one for each category.

When a categorical variable has k > 2 levels, we need to add k − 1 additional variables to the model.

Given the intercept term, we exclude one of the dummy variables from the regression.

The excluded variable represents the reference category. Example: Processing.Time Filtering by 3 categories: “Natural / Dry” “Washed / Wet“ or Other”) \(d_1=1\) for Other and 0 otherwise \(d_2=1\) for Washed/Wet and 0 otherwise \(d_1=d_2=0\) indicates Natural/Dry referent category

\(Score_i=β_0+β_1(I(Other)_i)+β_2(I(Wet)_i)+ϵ_I\) \(β_0\) represents the expected score for a coffee with 0 for the two dummy variables. That is, if it was a dry process coffee \(β_1\) represents the expected difference in score for coffee with an Other roasting process, compared to the baseline level (dry process) \(β_2\) represents the expected difference in score for Washed/Wet process coffee compared to dry process coffee. We have to estimate multiple “slopes” for this one variable - one corresponding to each non-reference level.

We can refilter the data to include the third category value.

coffee3cat <- filter(coffee, Processing.Method == "Natural / Dry" | Processing.Method ==

"Washed / Wet" | Processing.Method == "Other")

head(coffee3cat) X Species Owner Country.of.Origin

1 1 Arabica metad plc Ethiopia

2 2 Arabica metad plc Ethiopia

3 4 Arabica yidnekachew dabessa Ethiopia

4 5 Arabica metad plc Ethiopia

5 6 Arabica ji-ae ahn Brazil

6 7 Arabica hugo valdivia Peru

Farm.Name ICO.Number

1 metad plc 2014/2015

2 metad plc 2014/2015

3 yidnekachew dabessa coffee plantation

4 metad plc 2014/2015

5

6

Company Number.of.Bags Bag.Weight Harvest.Year

1 metad agricultural developmet plc 300 60 kg 2014

2 metad agricultural developmet plc 300 60 kg 2014

3 yidnekachew debessa coffee plantation 320 60 kg 2014

4 metad agricultural developmet plc 300 60 kg 2014

5 100 30 kg 2013

6 richmond investment-coffee department 100 69 kg 2012

Processing.Method Color Aroma Flavor Aftertaste Acidity Body Balance

1 Washed / Wet Green 8.67 8.83 8.67 8.75 8.50 8.42

2 Washed / Wet Green 8.75 8.67 8.50 8.58 8.42 8.42

3 Natural / Dry Green 8.17 8.58 8.42 8.42 8.50 8.25

4 Washed / Wet Green 8.25 8.50 8.25 8.50 8.42 8.33

5 Natural / Dry Bluish-Green 8.58 8.42 8.42 8.50 8.25 8.33

6 Washed / Wet Bluish-Green 8.42 8.50 8.33 8.50 8.25 8.25

Uniformity Clean.Cup Sweetness Cupper.Points Moisture Category.One.Defects

1 10 10 10 8.75 0.12 0

2 10 10 10 8.58 0.12 0

3 10 10 10 8.67 0.11 0

4 10 10 10 8.58 0.12 0

5 10 10 10 8.33 0.11 0

6 10 10 10 8.50 0.11 0

Quakers Category.Two.Defects unit_of_measurement altitude_low_meters

1 0 0 m 1950

2 0 1 m 1950

3 0 2 m 1800

4 0 2 m 1950

5 0 1 m NA

6 0 0 m NA

altitude_high_meters altitude_mean_meters TotalScore

1 2200 2075 90.58

2 2200 2075 89.92

3 2200 2000 89.00

4 2200 2075 88.83

5 NA NA 88.83

6 NA NA 88.75- We can make our new model object with the lm function.

lmModel2 <- lm(TotalScore ~ Processing.Method, data = coffee3cat)

summary(lmModel2)

Call:

lm(formula = TotalScore ~ Processing.Method, data = coffee3cat)

Residuals:

Min 1Q Median 3Q Max

-22.1346 -0.9646 0.4554 1.5354 8.6154

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 82.3541 0.1728 476.694 <2e-16 ***

Processing.MethodOther -1.0757 0.5639 -1.908 0.0567 .

Processing.MethodWashed / Wet -0.3895 0.1977 -1.971 0.0490 *

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 2.737 on 1086 degrees of freedom

Multiple R-squared: 0.005435, Adjusted R-squared: 0.003603

F-statistic: 2.967 on 2 and 1086 DF, p-value: 0.05186- The overall model is not significant here, but one group still shows differences. Means poor predictor, but that there are still group differences (even if small) between Washed/Wet and Natural/Dry

- Finally, we can make our new prediction of what the score would be in the Processing.Method was Other.

predict(lmModel2, data.frame(Processing.Method = "Other")) 1

81.27846 coef(lmModel2) (Intercept) Processing.MethodOther

82.3541434 -1.0756819

Processing.MethodWashed / Wet

-0.3895252 82.3541434 - 1.0756819[1] 81.27846Adding in a Numerical Variable

- We can add in another variable like Flavor. Flavor is a much stronger predictor.

lmModel3 <- lm(TotalScore ~ Flavor + Processing.Method, data = coffee3cat)

summary(lmModel3)

Call:

lm(formula = TotalScore ~ Flavor + Processing.Method, data = coffee3cat)

Residuals:

Min 1Q Median 3Q Max

-16.6648 -0.3555 0.2157 0.7248 5.7972

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 31.4116 1.0691 29.380 < 2e-16 ***

Flavor 6.7151 0.1403 47.849 < 2e-16 ***

Processing.MethodOther -0.1274 0.3205 -0.398 0.69108

Processing.MethodWashed / Wet 0.2931 0.1130 2.593 0.00964 **

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 1.553 on 1085 degrees of freedom

Multiple R-squared: 0.6802, Adjusted R-squared: 0.6793

F-statistic: 769.3 on 3 and 1085 DF, p-value: < 2.2e-16predict(lmModel3, data.frame(Flavor = 10, Processing.Method = "Other")) 1

98.43565 coef(lmModel3) (Intercept) Flavor

31.4116160 6.7151441

Processing.MethodOther Processing.MethodWashed / Wet

-0.1274019 0.2931262 31.411616 + 6.7151441 * 10 + -0.1274019[1] 98.43566- After adjusting for aroma, and flavor, is there sufficient evidence to suggest a difference in mean score between dry vs. wet process beans? Explain, using a formal hypothesis test. $H_0: Processing.Method_{Washed / Wet} = Processing.Method_{Dry} $ $H_A: Processing.Method_{Washed / Wet}Processing.Method_{Dry} $

lmModel4 <- lm(TotalScore ~ Aroma + Flavor + Processing.Method, data = coffee2cat)

summary(lmModel4)

Call:

lm(formula = TotalScore ~ Aroma + Flavor + Processing.Method,

data = coffee2cat)

Residuals:

Min 1Q Median 3Q Max

-17.5344 -0.2720 0.2208 0.7122 4.7629

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 28.1650 1.1482 24.530 < 2e-16 ***

Aroma 1.6013 0.2134 7.502 1.32e-13 ***

Flavor 5.5406 0.1987 27.884 < 2e-16 ***

Processing.MethodWashed / Wet 0.2337 0.1079 2.166 0.0306 *

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 1.479 on 1059 degrees of freedom

Multiple R-squared: 0.7017, Adjusted R-squared: 0.7009

F-statistic: 830.6 on 3 and 1059 DF, p-value: < 2.2e-16We find evidence that there is a difference between Washed/Wet processed coffee beans and dry processed beans as evident by the significant p-value < .05.

Adjusting for aroma, flavor, and process, which country has the highest expected score? The lowest?

## calculate the predicted scores in the dataset

predicted_scores <- predict(lmModel4, newdata = coffee2cat)

# Create a new dataframe with Country and predicted scores

predicted_data <- data.frame(Country = coffee2cat$Country, Predicted_Score = predicted_scores)

# Find the country with the highest expected score

highest_expected_score <- filter(predicted_data, Predicted_Score == max(Predicted_Score))

highest_expected_score Country Predicted_Score

1 Ethiopia 91.20569# Find the country with the lowest expected score

lowest_expected_score <- filter(predicted_data, Predicted_Score == min(Predicted_Score))

lowest_expected_score Country Predicted_Score

990 Guatemala 73.56705We find that Ethiopia has the highest predicted score and Guatemala has the lowest predicted score based on Aroma, Flavor, and Processing Method.

What percentage of the variability in the total score is explained by a linear relationship with the predictors in your model?

library(broom)

glance(lmModel4)# A tibble: 1 × 12

r.squared adj.r.squared sigma statistic p.value df logLik AIC BIC

<dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

1 0.702 0.701 1.48 831. 1.35e-277 3 -1922. 3854. 3879.

# ℹ 3 more variables: deviance <dbl>, df.residual <int>, nobs <int>- We can look at the R-squared value of .693 and adjusted R-squared value of .692 and state that about 69% of the variable in total score is explained by a linear relationship with the predictors in our model.

Assumptions of Linear Regression

Linear regression produces unbiased, efficient estimates and reliable significance tests only when a set of assumptions about the data and errors are reasonably satisfied. These assumptions apply to both simple and multiple regression. Violating them affects different things — some violations bias the coefficient estimates themselves, while others make the standard errors unreliable without changing the estimates.

What the Assumptions Are

Linearity means that the true relationship between each predictor and the outcome is linear — the expected value of \(Y\) changes by a constant amount for each one-unit increase in \(X\), all else equal. If the true relationship is curved, the slope estimate will average over different parts of the curve and be systematically wrong for some ranges of \(X\).

Independence of errors means that the residuals (\(e_i = y_i - \hat{y}_i\)) from one observation are not correlated with the residuals from any other observation. This is violated most commonly in time-series data (where observations from adjacent periods influence each other) and in clustered or hierarchical data. Correlated errors make standard errors too small, inflating t-statistics and producing false positives.

Homoscedasticity (constant variance of errors) means that the spread of residuals is approximately the same across all values of the predicted outcome. When the residuals fan out as \(\hat{y}\) increases (or decreases), the assumption is violated — a condition called heteroscedasticity. Heteroscedastic errors do not bias coefficient estimates, but they make standard errors unreliable, which invalidates hypothesis tests and confidence intervals.

Normality of errors means that the residuals are approximately normally distributed. This assumption is needed for the t-statistics on each coefficient and the F-statistic for the overall model to follow their theoretical distributions. With large samples, the CLT protects you and this assumption is less critical. With small samples, severely non-normal residuals can produce unreliable p-values.

No perfect multicollinearity means that no predictor is a perfect linear combination of the others. Perfect multicollinearity makes the model mathematically unsolvable (the matrix inversion fails). Near-perfect multicollinearity — the more common issue in practice — does not bias estimates but inflates standard errors, making predictors appear non-significant even when they genuinely predict the outcome.

What Happens When Assumptions Are Violated

| Assumption violated | Effect on estimates | Effect on inference |

|---|---|---|

| Non-linearity | Biased — wrong slope for parts of the range | Misleading predictions |

| Correlated errors | Unbiased | Standard errors too small; p-values too low |

| Heteroscedasticity | Unbiased | Standard errors unreliable; tests invalid |

| Non-normal errors | Unbiased (large samples) | p-values unreliable (small samples) |

| Multicollinearity | Unbiased | Standard errors inflated; predictors appear non-significant |

Visualizing the Homoscedasticity Assumption

The most important thing to check visually in regression is whether the residuals spread evenly across the range of fitted values — or whether they fan out (or fan in). The left panel shows well-behaved residuals; the right shows the classic funnel pattern that signals heteroscedasticity.

Residuals vs. Fitted Values — Homoscedasticity Check

In R, plot(your_lm_object) generates four diagnostic plots automatically, including residuals vs. fitted values and a Q-Q plot of residuals.

Testing Assumptions in R

R provides fast, accessible tools for checking all regression assumptions. The most efficient first step is the built-in plot() method for lm objects, which generates four diagnostic plots in sequence.

# Four diagnostic plots in one command

plot(your_lm_model)

# Plot 1: Residuals vs. Fitted — check linearity and homoscedasticity

# Plot 2: Q-Q plot of residuals — check normality

# Plot 3: Scale-Location — another homoscedasticity check

# Plot 4: Residuals vs. Leverage — identify influential observationsLinearity is assessed from the Residuals vs. Fitted plot: if the residuals form a random cloud around zero with no systematic curve, the linearity assumption is reasonable. A U-shape or wave pattern signals non-linearity.

Homoscedasticity is visible in both the Residuals vs. Fitted and Scale-Location plots. You can also run a formal Breusch-Pagan test:

library(lmtest)

bptest(your_lm_model) # p > .05: no significant heteroscedasticityNormality of residuals is assessed from the Q-Q plot. Points that closely follow the diagonal reference line indicate normally distributed residuals. For a formal test:

shapiro.test(residuals(your_lm_model)) # Works best for n < 5000Multicollinearity is diagnosed with VIF scores, as covered in the multicollinearity section above:

library(car)

vif(your_lm_model) # All values < 5: no problematic multicollinearity

When to be concerned vs. when to relax

Regression is robust to mild violations, especially with large samples. The hierarchy of concern is roughly: (1) multicollinearity deserves attention whenever VIF ≥ 10; (2) heteroscedasticity matters most for inference — use heteroscedasticity-robust standard errors (sandwich package) or a log transformation of Y if the funnel is pronounced; (3) non-normality of residuals matters most with small samples — it rarely causes problems when \(n > 100\); (4) non-linearity is the most serious because it means your slopes are wrong, not just your standard errors. Always check linearity first.

Review and Practice

Using AI

Use the following prompts in our chatbot below to explore more about regression analysis in R.

Understanding regression concepts:

Explain how to perform simple linear regression in R. Use the lm() function and discuss how to interpret the slope, intercept, and R-squared values from the regression output.

What is the coefficient of determination (R-squared) in regression analysis, and how does it relate to the goodness of fit? How can the residual standard error (RSE) and adjusted R-squared help in interpreting a model?

Describe how to perform multiple linear regression in R using the lm() function. How do you interpret the coefficients for multiple predictors, and what do the p-values tell you about their significance?

What does the F-statistic in a regression output indicate? How does it help in determining the significance of a regression model, and what role does it play when comparing multiple models?

Explain how ANOVA is related to regression analysis. How can the F-test be used to assess the significance of regression models? What are residuals in a regression model, and how can analyzing them help assess model fit? How is the sum of squared errors (SSE) related to residual analysis?

What is multicollinearity, and why is it problematic in multiple regression? How can you detect multicollinearity in R using the vif() function, and what steps can be taken to address it?

How can you use a fitted regression model to make predictions for new data in R? Explain how the predict() function works and provide an example using both simple and multiple regression.

Given the output from the summary() function for a regression model in R, explain how to interpret the coefficients, R-squared, adjusted R-squared, residual standard error, and p-values.

Describe how to use the p-value method for variable selection in multiple regression. How do you iteratively remove insignificant predictors while monitoring the R-squared and adjusted R-squared values?

Prompting AI effectively for regression tasks:

| Vague prompt | Specific prompt |

|---|---|

| “Run a regression” | “Run a multiple regression predicting home_value from season, year, and income_needed in zillow.csv. Use lm(), print summary(), interpret the Adjusted R², and explain which predictors are significant at α = 0.05. Check for multicollinearity using vif() from the car package and flag any VIF values above 5.” |

| “What does this output mean?” | “I ran summary(lm(home_value ~ season + income_needed, data=zillow)) and got these results: [paste output]. Explain what the Intercept, seasonSpring coefficient, income_needed coefficient, and p-values mean in plain English for a non-statistician. Do not use causal language — describe these as associations, not causes.” |

| “Make a prediction” | “Using my fitted regression model m1 <- lm(home_value ~ income_needed, data=zillow), write code using predict() to forecast home_value for a new observation where income_needed = 85000. Include a 95% prediction interval.” |

Verification checklist for AI-generated regression output:

After AI generates a regression model and interpretation, check four things: (1) do the coefficient signs make intuitive sense — if the model says higher income needed is associated with lower home values, something is wrong; (2) is the Adjusted R² reasonable for your domain — a value of 0.95 for economic data should raise questions; (3) did AI flag any multicollinearity concerns, or do you need to run vif() yourself; (4) does AI’s interpretation use causal language (“X drives Y,” “X causes Y”) when the model only supports associational language (“X is associated with Y,” “a one-unit increase in X predicts a Y-unit change in the outcome”)? Correct causal language to associational language before presenting results to any audience.

Regression Lab

A dataset has one continuous predictor variable (Income, in thousands) and one continuous outcome (Debt, in dollars). A student runs lm(Debt ~ Income, data = df) and gets the following summary output:

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 210.30 41.82 5.03 0.00004 ***

Income 10.44 1.19 8.77 9.66e-09 ***

Residual standard error: 63.26 on 26 degrees of freedom

Multiple R-squared: 0.7526, Adjusted R-squared: 0.7423

F-statistic: 76.86 on 1 and 26 DF, p-value: 9.66e-09Write out the regression equation, interpret the slope and intercept in plain English, and state what the \(R^2\) tells you about model fit.

Show Answer

Regression equation: \[\hat{y} = 210.30 + 10.44 \times \text{Income}\]

Intercept (\(b_0 = 210.30\)): When Income is zero (i.e., $0 in thousands), the predicted debt payment is $210.30. In this context, the intercept is a mathematical anchor for the line — there is likely no data at Income = 0, so it should not be interpreted as a meaningful real-world value on its own.

Slope (\(b_1 = 10.44\)): For every additional $1,000 in income (one unit increase in Income), debt payments are predicted to increase by $10.44. Income and debt move in the same direction — higher earners tend to carry higher debt payments.

\(R^2 = 0.7526\): Income explains approximately 75.3% of the variability in debt payments. The remaining 24.7% is explained by other factors not in the model. An \(R^2\) above 0.5 is generally considered moderate-to-strong in business applications — this model fits the data reasonably well.

Using the regression output above, make a prediction for a person with an income of $85,000 (Income = 85) using both the regression equation and the predict() function in R. Show both approaches.

Show Answer

Using the equation: \[\hat{y} = 210.30 + 10.44 \times 85 = 210.30 + 887.40 = 1097.70\]

Predicted debt payment: approximately $1,097.70

Using predict() in R:

predict(Simple, data.frame(Income = 85))Both approaches give the same answer. The predict() function is more convenient when making many predictions at once or when the model includes multiple predictors, since it handles all the coefficient multiplication automatically.

A multiple regression model is built to predict Balance from Income, Rating, Limit, Cards, Age, and Education. The initial model returns the following Adjusted \(R^2\) values as variables are removed one at a time using the p-value method:

| Step | Variables removed | Adjusted R² |

|---|---|---|

| 0 (full model) | — | 0.8764 |

| 1 | Education (p = 0.71) | 0.8765 |

| 2 | Cards (p = 0.53) | 0.8760 |

| 3 | Age (p = 0.06) | 0.8753 |

| 4 | Limit (p = 0.059) | 0.8745 |

Explain why Adjusted \(R^2\) barely changes — and in step 1 actually increases — as variables are removed, and why this supports the variable-removal decisions.

Show Answer

Why Adjusted \(R^2\) barely changes: The variables being removed (Education, Cards, Age, Limit) were contributing almost nothing to the model’s explanatory power. When a predictor is truly uninformative, removing it does not reduce how well the model fits the data — it just eliminates noise.